在Wash Sale详解一文中我们介绍了wash sale的基本规则。想必读者已经熟悉以sale at loss去找对应的replacement share,然后调整cost basis和holding period的过程了。

本文我们介绍三种常见的wash sale错误。之所以叫错误,是因为这些wash sale不易发觉,或有略特殊的税法规定。它们分别是dividend reinvestment, related party transaction以及IRA wash sale。

本文会分别介绍原理和应对方法。

Contents

Dividend Reinvestment

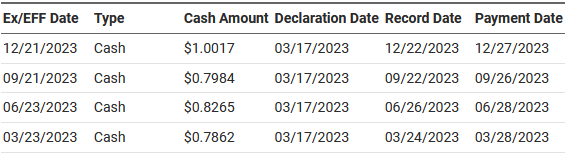

投资共同基金或EFT会产生dividend,这在指数基金中尤其常见。下表为vanguard的指数基金VTI在2023年的dividend payment

表中Ex Date/Record Date解读可参考文章分红税务中的Holding Period与Qualified Dividends。

投资人如果长持该股,特别是buy and hold策略,则往往会选择将dividend重新投资到该股中。为了省却手动操作的麻烦,很多券商会提供automatic dividend reinvesement功能,例如下图是Fidelity账户中Dividend reinvesement设置页面:

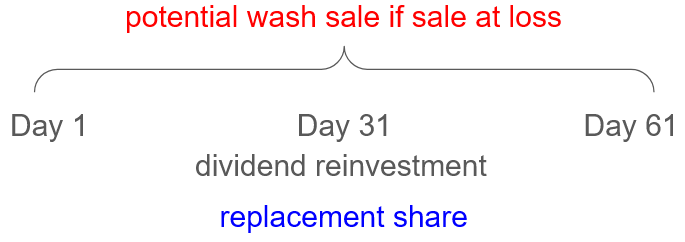

选择Reinvest in Security,只要dividend在Payment date出现,就会立即买入同一投资品。如果在前后30天内有同一投资品卖出,那么dividend reinvestment就会出现在这次买出的前后30天内,卖出变成wash sale,dividend reinvestment变成replacement share,需要调整cost basis。

Dividend通常占比不大,但因为automatic reinvestment很容易忽视,让投资人往往没有意识到wash sale的存在。但正因为dividend数量少,由之引起的disallowed loss也少,只是若不在同一券商,报税时这些不大的disallowed loss也要花时间寻找。

若想避免这个麻烦,我们建议

-

关闭dividend automatic investment,改成手动,用与其他投资一样的方式避开wash sale。对于定投指数基金的策略,一年一次与一季度投一次收益差别很小。

-

或者在卖出、或者准备做tax loss harvesting时,关闭dividend automatic investment,过31天后再打开。

-

或者不同的券商买不同的投资品。

Related Party Transaction

第二种情况,是投资人利用related party(相关方)买下replacement share,以规避wash sale rule,但这同样会造成disallowed loss,而且后果比wash sale更严重。

Related Party

根据publication 550,这里的related party可以是家庭成员(包括直系亲属:兄弟姐妹,父母祖父母,子女)

Members of your family. This includes only your brothers and sisters, half-brothers and half-sisters, spouse, ancestors (parents, grandparents, etc.), and lineal descendants (children, grandchildren, etc.).

以及直接或间接控股50%以上的公司、公司合伙人等。

历史上有这样的失败避税案例。Shoenberg通过自己控制的公司Globe Investment Company购买replacement share,被法院判定loss disallowed(Shoenberg , 77 F.2d 446 (8th Cir. 1935))。McWilliams则是通过妻子购买replacement share而被最高法判定loss disallowed(McWilliams v. Commissioner, 331 U.S. 694 (1947))。

姻亲(in-law)按定义不是related-party,但也要看州法律规定

In-laws are not related parties under Sec. 267, and, therefore, using an in-law to purchase stock or securities may accomplish a taxpayer’s goal of retaining control and recognizing the loss on the sale of the stock. In community property states, spouses generally each own half of marital property. In those states, using an in-law to avoid the wash-sale rules may be effective for only half of the loss.

Sec. 267

Related party transaction适用范围不仅限于wash sale(IRC Sec. 1091)。其在IRC Sec. 267中另有Deduction for losses disallowed条款

(1) Deduction for losses disallowed

No deduction shall be allowed in respect of any loss from the sale or exchange of property, directly or indirectly, between persons specified in any of the paragraphs of subsection (b). The preceding sentence shall not apply to any loss of the distributing corporation (or the distributee) in the case of a distribution in complete liquidation.

与IRC Sec. 1091囊括的wash sale不同,Sec. 267首先不受时间61天的时间窗口限制,其次也没有cost basis调整过程,只有最终卖出后有收益,才能抵掉前面的亏损:

you recognize the gain only to the extent that it is more than the loss previously disallowed to the related party

看publication 550的例子,

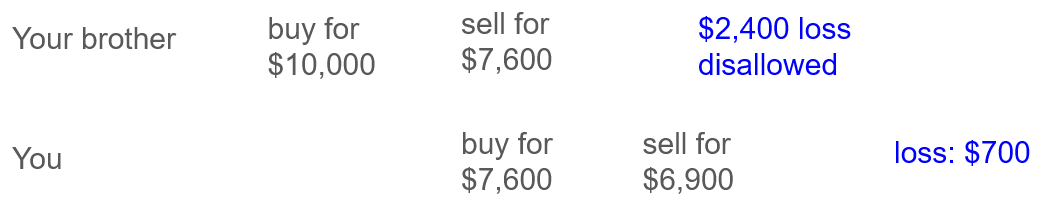

Example 1. Your brother sells you stock for $7,600. His cost basis is $10,000. Your brother cannot deduct the loss of $2,400. Later, you sell the same stock to an unrelated party for $10,500, realizing a gain of $2,900. Your reportable gain is $500 (the $2,900 gain minus the $2,400 loss not allowed to your brother).

(姑且认为是)哥哥的股票亏损2400,买给弟弟,由于是related-party transaction,哥哥无法将这2400算做loss抵税。弟弟若最终盈利2900,则弟弟报税时可以抵掉2400的损失,盈利变成500。

Example 2. If, in Example 1, you sold the stock for $6,900 instead of $10,500, your recognized loss is only $700 (your $7,600 basis minus $6,900). You cannot deduct the loss that was not allowed to your brother.

但若弟弟卖出时也是亏损700,那么兄弟俩原来的2400损失就凭空消失了,弟弟不能将损失报成3100。

Prearranged plan

McWilliams , 331 U.S. 694 (1947)认为McWilliams的related party交易属于预谋(prearrangement),不能抵税。若纯属巧合也许可以豁免:

Indirect transactions. You cannot deduct your loss on the sale of stock through your broker if, under a prearranged plan, a related party buys the same stock you had owned. This does not apply to a trade between related parties through an exchange that is purely coincidental and is not prearranged.

Prearranged没有标准界定。和法律中其他意图判断一样,要看文本证据,具体的交易细节,IRS的监管力度,和法庭的风向等。

对于广大读者最常见的亲人间交易来说,实控亲人账户,交易时间间隔非常短,父母与小家庭经济往来密切,那么判为预谋的可能性大。 不同的household,没有经济往来的兄弟姐妹,则判为巧合的可能性大。Plus1s认为对于同一家庭的成员,定期交流投资计划,避免related party transaction为好。或没有家庭成员间很少往来(兄弟分家),也无需刻意打听。

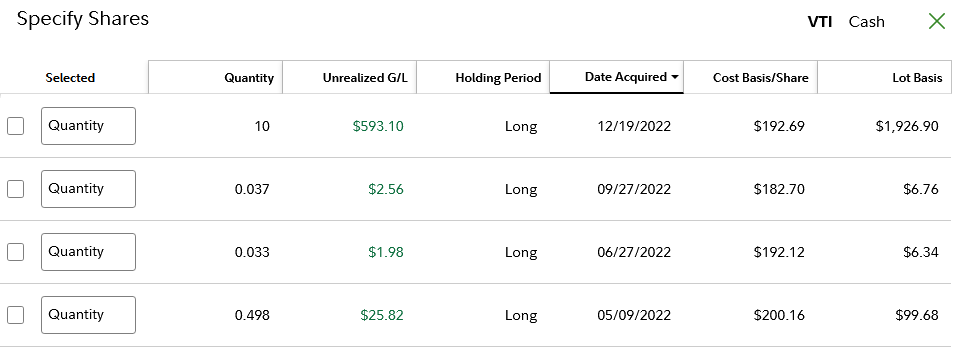

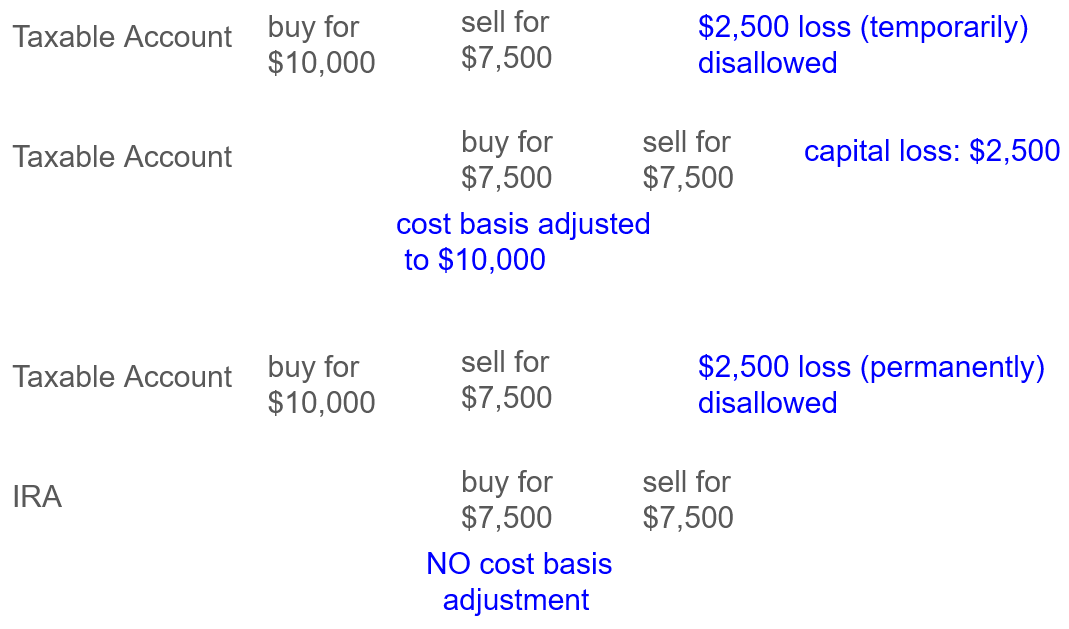

尽管很多券商会在IRA内也记录每一项投资的cost basis,以及holding period,例如下图是plus1s持有的HSA中VTI的tax lot:

但从IRA中取钱时,税务计算与投资的cost basis/captial gain无关(参考tranditional IRA与Roth IRA介绍),所以wash sale的cost basis adjustment没有效果。

2007年底,IRS发布了关于涉及IRA wash sale的Rev. Rul. 2008-5,

- 它首先明确了在IRA中买回replacement share也是wash sale,不是漏洞。

- 其次IRA内cost basis adjustment无需调整。

- 其附带结果为,disallowed loss不是延迟而是永久消失。

下图的两个例子展示了这一对比:

结合本文探讨的第一种错误,当IRA内的投资开启dividend reinvestment时,投资者可能不知不觉陷入了IRA wash sale的陷阱,dividend reinvestment对应部分的loss就永久失去了。为了避免,建议IRA的投资尽量与taxable account不同。

尽管没有其他Revenue Ruling,其他诸如401(k), 457(b)的账户原理与IRA相同,其cost basis调整也没有意义。有理由认为如果这些账户买入了replacement share,也会造成loss永久消失。

总结

本文介绍了三种常见的wash sale错误:dividend reinvestment, related party transaction以及IRA wash sale。但只要

- 关停dividend reinvestment或者卖出时检查

- 与亲近的家庭成员间互相知会重要交易的细节

- IRA以及其他退休账户与taxable account保持投资品类不同

即可规避。

参考资料:publication 550; Tradelog: IRS Wash Sale Rule; Fairmark: Wash Sale Rule;

The Tax Advisor: Preserving Tax Losses by Avoiding the Wash-Sale Rules

免责声明:本文及其中任何文字均仅为一般性的介绍,绝不构成任何法律意见或建议,不得作为法律意见或建议以任何形式被依赖,我们对其不负担任何形式的责任。我们强烈建议您,若有税务问题,请立即咨询专业的税务律师或税务顾问。

Disclaimer: This article and any content herein are general introduction for readers only, and shall not constitute nor be relied on as legal opinion or legal advice in any form. We assume no liability for anything herein. If you need help about tax, please talk to a tax, legal or accounting advisor immediately.