股份公司盈利之后,可根据规则派发部分盈利给股东,这就是dividend,中文译为股息或分红。若不是直接持有公司,最常见的获取分红的方式是持有上市公司股票。传统的观点,公司在上升阶段更倾向于将盈利用于扩大生产,故分红少或不分红;公司在成熟阶段用分红向股东展示盈利能力和财务状况。但近几十年兴起的科技企业普遍选择不分红,它们有盈利时也选择回购(stock buyback)拉高股价。

本文不分析分红的利弊,只讨论dividend的现行税务规则。

Dividend原先与ordinary income相同。2003年通过的Jobs and Growth Tax Relief Reconciliation Act创造了qualified dividend的概念。与资本税(captial gain tax)类似,长持的股票,产生的分红以长期资本税率缴税,而短期持有则适用收入税。

分红的holding period规则与资本税不同,在1040税表上也与资本税不在一处。本文介绍关键日期ex-dividend date,holding period以及qualified dividend的概念。希望读完本文,可以理解1040 Line 3上关于dividend的处理。

Contents

Ex-dividend date

公司公布某日期派发dividend,何时买入这个公司的股票才可以拿到dividend呢?

对于投资人来说,公司会对每一笔dividend会公布一个重要日期:

ex-dividend date: definition from wikipedia

The ex-date or ex-dividend date represents the date on or after which a security is traded without a previously declared dividend or distribution.

假如购买日期在ex-dividend date当天或之后,买家无法拿到下一次dividend(即ex-dividend date对应的那次dividend),而卖家可以。

Ex 在这里的意思是excluding:

ex: [Oxford Language] British: without; excluding.

想要拿到dividend,必须在ex-dividend之前买入。

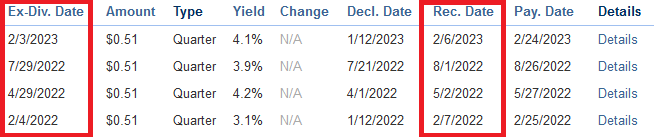

例子:Bestbuy(BBY)在2022年的4个ex-dividend date:

这里除了ex-dividend date之外,还有公司宣布dividend的日期(declaration date),支付dividend的日期(payment date),以及公司与ex-dividend date相关的record date。

Record date

对于公司来说,只有record date这一天出现在记录中的股东才可以拿dividend。在美国,stock和ETF的settlement delay是2天,trade之后2天才settle(T+2)。若在record date至少两个交易日之前买入,则settlement date一定是在record date当日或之前,于是可以拿到本期dividend。于是根据定义,公司将股票的ex-dividend date设置在record date之前的一个交易日。

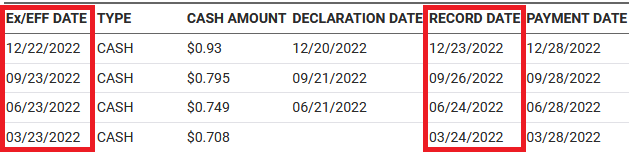

若record date是周一,则ex-dividend是上一个周五。Citigroup(C)的ex-dividend date即是如此:

Declared date vs payment date

一般情况下,这两个日期不重要。但如果这两个日期跨年了,根据publication 550

Dividends received in January. If a mutual fund (or other regulated investment company) or real estate investment trust (REIT) declares a dividend (including any exempt-interest dividend or capital gain distribution) in October, November, or December, payable to shareholders of record on a date in one of those months but actually pays the dividend during January of the next calendar year, you are considered to have received the dividend on December 31. You report the dividend in the year it was declared.

税务上以Declared date所在年的最后一天作为收到dividend的日期。

ETF与mutual fund

若ETF和mutual fund所控制的股票产生dividend,则这些dividend会通过ETF和mutual fund传递给投资者。一般是每季度分发一次,例如vanguard的指数基金VTI

及其对应的mutual fund: VTSAX:

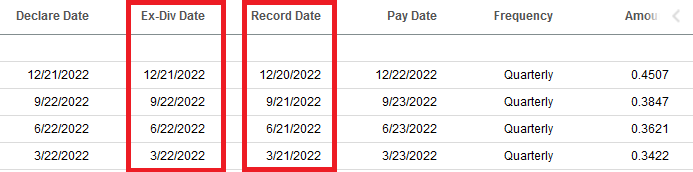

一个奇怪的现象:为什么VTSAX的ex-dividend date反而比record date晚一天呢?

这是因为mutual fund是在trading day结束之后交易,根据当日的net asset value定出的价格成交。买入这一天就出现在的股东的记录上,所以ex-dividend date根据定义是record date的下一个交易日。可见ex-dividend date与交易规则和settlement cycle有关。

对于税务问题,我们只需要关注ex-dividend date。

Qualified dividend/Non-qualified dividend

Qualified dividend可以享受较低的long-term captial gain tax rate的待遇。Qualified的条件粗略地讲,一是美国公司派发,二是要满足holding period。详细精确的规则事实上包含domestic corporations和qualified foreign corporations,以及还有一些其他的excpetions,具体请查询Form 1099 DIV instructions。

Holding period

You must have held the stock for more than 60 days during the 121-day period that begins 60 days before the ex-dividend date.

以ex-dividend date为中心前后60天,一共121天的时间里,至少持有61天。

举一个fidelity网站上的例子:

股票S的ex-dividend date是May 2。其121天的区间是March 3 – July 1。

When counting the number of days you held the stock, include the day you disposed of the stock, but not the day you acquired it.

Holding period的先决条件是ex dividend date之前有买入,这样才能拿到dividend。如果May 2买入,即使持有到July 1也只持有了60天。

Fidelity给的例子是April 27购入10k shares,June 15卖掉2k shares,剩下的8k shares一直持有到July 1之后。

那么June 15卖掉的2k shares在这121天中的持有时间是49天(April 28 through June 15),这部分dividend是non-qualified dividend。而剩余的8k shares持有时间超过60天(from April 28 through July 1),它产生的dividend是qualified dividend。

一些例外规则:

- 假如有一些hedge措施(例如做空)使得持有风险降低,则不计入holding period;只有unhedged position才计入holding period

- 以上holding period要求是针对普通股(common stock),优先股(preferred stock)的holding period的要求变成ex-dividend date前后90天的181天区间内至少持有91天

不满足条件的non-qualified dividend按照income缴税。

Form 1099-DIV, Form 1040 example

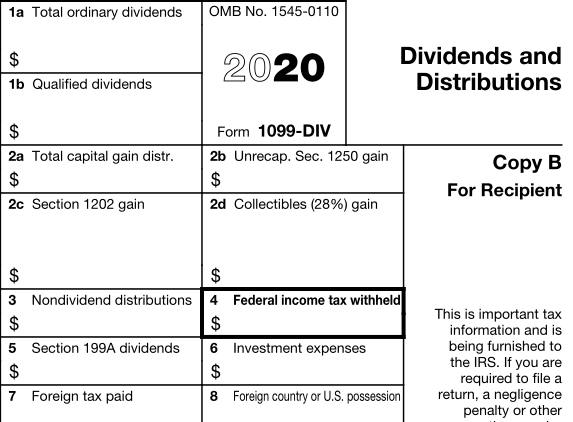

券商在第二年年初会将dividend的情况汇总到1099-DIV,分别寄给税务部门和投资人。券商帮助投资人计算holding period,将满足条件的qualified dividend计入Box 1b。Dividend总数计入Box 1a。前一节holding period的计算理解大意即可,券商会帮忙计算。

我们注意到Fidelity网站上有一段说明,Box 1b未必就全是qualified,

Qualified dividends are reported on Form 1099-DIV in line 1b or column 1b. However, not all dividends reported on those lines may have met the holding period requirement. Those non-qualified dividends, as well as other ordinary dividends, may be taxed at your ordinary income tax rate, which can be as high as 37%.

这主要是因为fidelity作为一家券商,不可能知道投资者所有的position。投资人完全可以在fidelity处投资股票,在另一家券商做空这只股票降低风险。按照前述holding period的例外规则,有hedge的时间不可以计入holding period。这样fidelity给出的1099-DIV表格可能出现偏差。这种情况类似于不同券商之间的wash sale,需自行计算更正。

Box 5当中的199A dividends来自于REIT。虽然这不是qualified dividend,但2017年通过的TCJA规定,可以有20%的qualified business income deduction。填写Form 8995即可。

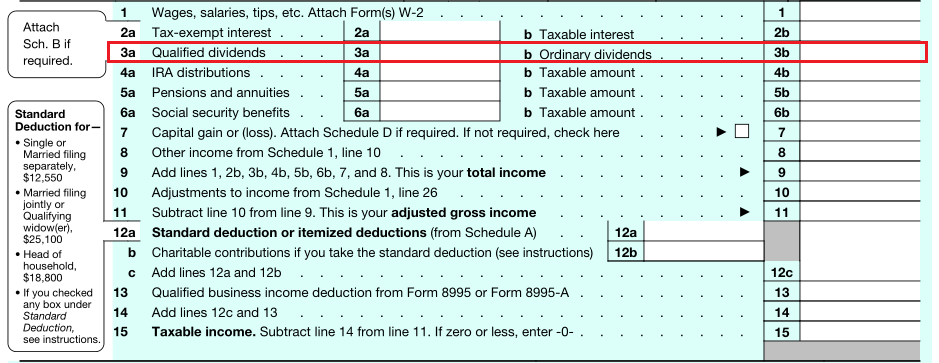

在1040表中,将qualified dividend填入Box 3a(对应1099-div Box 1b),将dividend总额填入Box 3b(对应1099-div Box 1a)。

1040上Line 3b是否重复缴税?名词辨析: ordinary dividend

坊间流传一种说法是ordinary dividend按照ordinary income交税,qualified dividend按照long term captial gain交税。甚至IRS的Topic No. 404 Dividends也是这样说:

Whereas ordinary dividends are taxable as ordinary income, qualified dividends that meet certain requirements are taxed at lower capital gain rates.

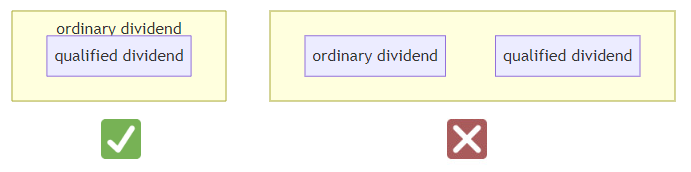

这容易让人认为ordinary dividend与qualified dividend是互斥的。即,如果某项dividend是ordinary dividend,那么就不可能是qualified dividend。

但是Form 1099-DIV的instruction却告诉我们

Box 1b. Qualified Dividends

Enter the portion of the dividends in box 1a that qualifies for the reduced capital gains rates.

也就是说Box 1b的qualified dividend是Box 1a Total ordinary dividend的一部分。Publication 550中qualified dividend也是如此:

Qualified dividends are the ordinary dividends subject to the same 0%, 15%, or 20% maximum tax rate that applies to net capital gain

但这样理解的话,1040表中计算total income时,dividend用的是Line 3b,也就是total dividend,是不是qualified dividend也被算在total income里面,交了收入税呢?或者既交了一遍收入税,又交了一遍资本税?

Turbo Tax论坛上也有人提出了这个问题。

我的解答是这样的:

- Qualified dividend在1099-DIV Box 1a以及1040 Line 3b中都是ordinary dividend的一部分,即Publication 550中定义的含义。IRS在1099-DIV中使用了Total ordinary dividend以示强调这是所有的dividend总和。

- 在1040中计算总收入时,所有dividend(qualified or not)都会并入计算。所以total income, adjusted gross income (AGI), taxable income 全部包含qualified dividend。

用AGI决定IRA的存入上限,以及其他一些tax credit的时候,qualified dividend和long term captial gain一样,都是income的一部分。

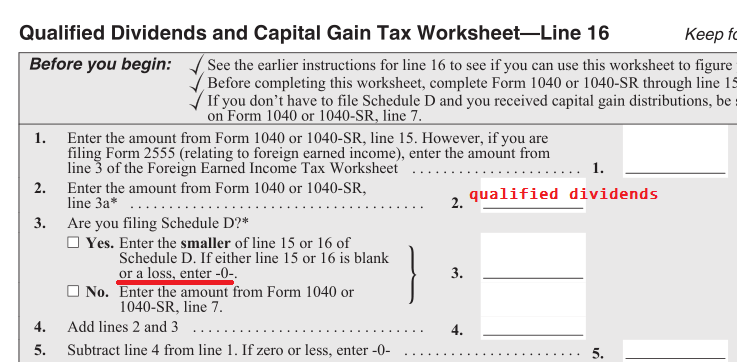

- qualified dividend的税率是long term capital gain rate。这是通过1040的Qualified Dividends and Capital Gain Tax Worksheet—Line 16实现的。

Line 15/16中小的那一行是long term capital gain/loss。如果有capital loss的话,就只计算qualified dividend的long term capital gain tax;如果long term capital gain的计算结果为正,则加在其上面。

这一操作说明,captial loss不能抵消qualified dividend。

我们应将qualified dividend理解为一种按long term capital gain bracket征税的income,但不能等效成long term capital gain。

1040表格并没有重复征税,对qualified dividend的税率使用也是正确的。

- 我认为ordinary dividends的命名有歧义。IRS自己在Topic No. 404使用了其错误定义,导致错误蔓延到investopedia的ordinary dividend页面:

Retrived date: 01/14/2023

Ordinary dividends are taxed as ordinary income, while qualified dividends are taxed at the lower capital gains rate.

我建议在平常交流时使用qualified dividend/non-qualified dividend。

认为ordinary dividend这个名称不妥的,可以在这个网址向IRS反映他们表格术语的问题。

总结

本文介绍了dividend税务规则。Ex-dividend date决定了获取dividend的买入时间,其前后60天的121天窗口决定了Holding period。最后,本文还展示了1099-DIV以及1040表格上qualified/ordinary dividends出现的位置,它们参与总税额计算的过程,以及ordinary dividend这一术语的歧义。

阅读本文后,读者在报税时,应能理解dividend tax的含义了。

参考资料:publication 550; wiki: Ex-dividend date, wiki: Quanlified dividend; fidelity: qualified dividend

免责声明:本文及其中任何文字均仅为一般性的介绍,绝不构成任何法律意见或建议,不得作为法律意见或建议以任何形式被依赖,我们对其不负担任何形式的责任。我们强烈建议您,若有税务问题,请立即咨询专业的税务律师或税务顾问。

Disclaimer: This article and any content herein are general introduction for readers only, and shall not constitute nor be relied on as legal opinion or legal advice in any form. We assume no liability for anything herein. If you need help about tax, please talk to a tax, legal or accounting advisor immediately.