Roth 401(k)是一個401(k) plan中廣泛存在的子賬戶。俗名來自於Roth IRA與401(k)的結合,意指存入稅後金額(Roth),但退休後取出時免稅的401(k)選項。

Roth 401(k)兼有Roth IRA與401(k)的特點,但又不完全等同。本文介紹Roth 401(k)相關的存入取出規則。立法技術上,Roth 401(k)是對pre-tax 401(k)相關條款的增補。諸如elective deferral, vesting schedule等401(k)共通特性,本文不再詳述,請先參考閱讀401(k)綜述。由於in-plan Roth rollover規則複雜,本文暫不涉及,今後將專文介紹。

Contents

(Designated Roth) Contribution

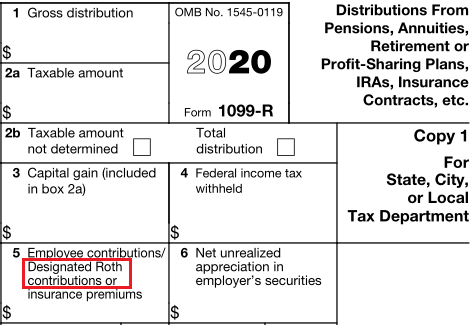

Roth 401(k)的標準名稱為designated Roth account,這一專有詞彙經常出現在1099-R、Form 8606等稅表及其instruction中。

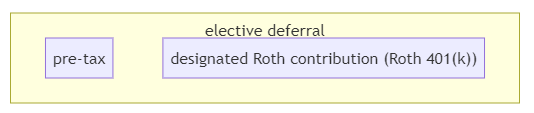

401(k) plan的elective deferral在2006年以前完全是pre-tax。2001年的法案為elective deferral提供了Roth選項:從2006年起,401(k) plan允許參與者指定一部分elective deferral為after-tax,存入的after-tax金額即為參與者的designated Roth contribution。與pre-tax 401(k)一樣,僱主可根據員工的設定,從每期的paycheck中扣除後存入。

據此,Roth 401(k)並不是單獨的401(k) plan,而是整個401(k) plan中的獨立記賬的子賬戶。因為其稅務規則類似於Roth IRA,designated Roth account一般俗稱為Roth 401(k)。

由designated Roth contribution的定義,Roth 401(k)與pre-tax 401(k) contribution分享elective deferral的限額。兩者存入總額(包含所有401(k) plan)不能超過402(g) limit(即elective deferral limit,見401(k)綜述)。同樣,Roth 401(k) contribution作為elective deferral的一部分,不可以做in-service distribution,在職期間無法取出。

在不考慮in-plan Roth rollover的情況下,Roth 401(k)的賬目分為兩個部分:

| Roth 401(k) funds | note |

| designated Roth contribution | deposit in each pay period |

| earning | what remains in Roth 401(k) |

類似於Roth IRA賬目中的Roth regular contribution,designated Roth contribution是Roth 401(k)的basis,即本金。

Withdraw/Distribution

pro-rata rule

Roth 401(k)是401(k)的子賬戶,取出操作遵循401(k)的基本規則,即pro-rata rule:與traditional IRA一樣,basis與earning會被成比例取出。

qualified distribution

Basis部分取出時免稅(return of basis),earning部分的稅務後果取決於兩個條件

5-taxable-year period of participation: 該Roth 401(k)的第一筆contribution已超過5年- 滿足其他任意一個

qualified distribution條件,常見的條件是所有者年齡超過59.5歲

排列組合見下表(與Roth IRA相同):

| 小於59.5歲 | 超過59.5歲 | |

| Roth 401(k)持有小於5年 | 收入稅 ✅ 10%罰金✅ | 收入稅 ✅10%罰金 ❎ |

| Roth 401(k)持有超過5年 | 收入稅 ✅ 10%罰金✅ | 收入稅 ❎10%罰金 ❎ |

5-taxable-year period of participation

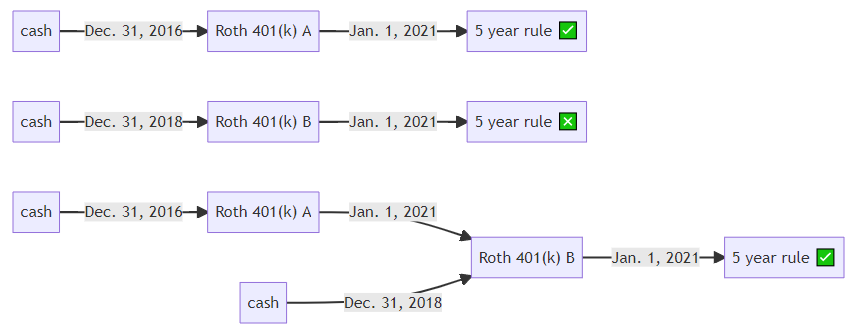

這是Roth 401(k)的第一個五年規則,從第一筆designated Roth contribution所在的那個tax year開始計時,連續5年。這與Roth IRA的5-year non-exclusion period類似,但有如下不同

- 不同僱主的Roth 401(k)分開計時

- 發生

Roth 401(k) -> Roth 401(k)direct rollover時,如果第一個plan(即rollover移出資金的plan)存入早,則第二個plan(即rollover移入資金的plan)的5年計時會被提前成第一個plan的計時(CFR Sec. 408A-10 Q2 A2 (b))。

例子:假設Craig於2016年12月31日第一次存入僱主A的Roth 401(k),金額5k (避免involuntary cash out)。則Roth 401(k) A的5年規則計時開始的年份為2016年(tax year),至2021年1月1日滿足5年規則。假設Craig於2018年1月1日第一次存入僱主B的Roth 401(k),則2021年1月1日,僱主B的Roth 401(k)的5年規則計時只有3年。但若2021年1月1日,Craig做一次Roth 401(k) A -> Roth 401(k) B direct rollover,則Roth 401(k) B的首次存入時間會被重置為2016年12月31日,當即滿足5年規則。反過來Roth 401(k) B -> Roth 401(k) A的rollover不會重置Roth 401(k) A的首次存入時間,因為Roth 401(k) A的首次存入時間更早。

注意:Roth IRA的5-year non-exclusion period不存在每個IRA的單獨計時(aggregation),只考慮所有IRA中的第一個。

required minimal distribution

這是Roth 401(k)另一與Roth IRA的不同點:Roth 401(k)有RMD,持有人滿72歲後要按照IRS提供的預期壽命的表格計算每年最低取出的比例,否則少取部分有50%的罰金。

但Roth 401(k)的RMD可以通過Roth 401(k) -> Roth IRA避免。

Rollover

本文暫不考慮in-plan Roth rollover,這樣涉及Roth 401(k)的rollover只有兩種

Roth 401(k) -> Roth 401(k)

Roth 401(k) -> Roth IRA

從Roth 401(k)中移出的資金,首先按pro-rata rule計算出basis與earning。對於第一種rollover,basis和earning與目的地的Roth 401(k)賬目合併。

對於第二種rollover,CFR Sec. 408A-10 Q3 A3以Q&A形式明確回答了Roth 401(k)的basis應視作Roth IRA的regular contribution。也即我們有如下賬目的對應關係:

| Roth 401(k) | –> | Roth IRA |

| designated Roth contribution | –> | regular contribution |

| Roth 401 (k) earning | –> | Roth IRA earning |

這樣,通過離職後的Roth 401(k) -> Roth IRA rollover,員工可以地避免Roth 401(k)的pro-rata rule以及RMD。當Roth 401(k)的basis進入Roth IRA之後,變成了可以隨時取的Roth IRA regular contribution,而Roth IRA沒有RMD。

split rollover

在做Roth 401(k) -> Roth 401(k)/Roth IRA rollover時,可以留下一部分現金,只將剩餘部分移入目的地的Roth 賬戶,此時CFR Sec. 402A-1 Q5 A5規定rollover移入的資金先計算earning部分。這樣split rollover也是一個避開pro-rata rule,從Roth 401(k)中取本金的方法。

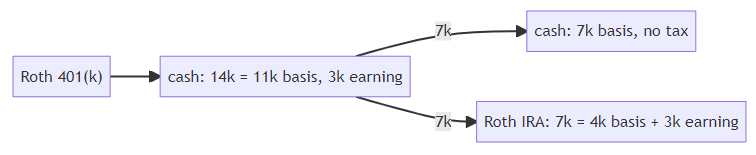

例子:Lisa從僱主A的Roth 401(k)中取出14k,其中包含11k basis與3k earning。當她只將7k移入自己的Roth IRA時(以indirect rollover形式),3k是earning, 4k是basis,剩餘在手的7k現金全是afer-tax basis。這樣即使她不滿59.5歲,也不用對earning部分交收入稅和罰款,因為earning已經全部進入Roth IRA。

根據CFR Sec. 402A-1 Q5 A5 (c),此種indirect rollover中,Lisa也可以將3k earning移入另一個僱主B的Roth 401(k),但此時僱主B Roth 401(k)的5-year non-exclusion period計時不會提前。注意Lisa取出Roth 401(k)的資金再rollover的操作屬於indirect rollover,而前文Craig的例子中Roth 401(k) -> Roth 401(k)中引起計時提前的操作是direct rollover(兩者區別見此文開頭)。

Pre-tax 401 (k) vs Roth 401 (k)

兩者關於稅務優勢的比較與traditional IRA vs Roth IRA相同(traditional IRA vs Roth IRA),經典結果為

- 如果當前稅率高,存pre-tax 401(k)有利

- 如果退休時稅率高,存Roth 401(k)有利

其他方面的比較如下表,

| tax benefit | contribution limit | distribution rule | RMD | |

| pre-tax 401(k) | pre-tax contribution, tax-deferred growth | 402(g) limit (shared with Roth 401(k)) | qualified distribution | Yes |

| Roth 401(k) | after-tax contribution, tax free growth | 402(g) limit (shared with pre-tax 401(k)) | 5-year participation period, pro-rata rule (but can be avoided via -> Roth IRA), qualified distribution | Yes (but can be avoided via -> Roth IRA) |

總得來說,Roth 401(k)在離職時結合-> Roth IRA變得更靈活。本文作者建議視個人情況調整pre-tax/Roth 比例,不建議只存其中一種,以免新法規帶來變數。

總結

Roth 401(k)是401(k)中大體遵照Roth存取規則的子賬戶(例外規則為pro-rata rule, RMD),其與pre-tax 401(k)的比較大體與traditional IRA vs Roth IRA相同,見文中表格總結。請視個人情況設定pre-tax/Roth比例。

Roth 401(k) -> Roth IRA rollover可避免Roth 401(k)的pro-rata rule和RMD,是離職時可考慮的選項;若新僱主仍提供Roth 401(k),也可考慮使用Roth 401(k) -> Roth 401(k) (direct) rollover縮短或立即滿足新Roth 401(k)的5-taxable-year period of participation要求。

參考資料:IRC Sec. 402A, CFR Sec. 402A-1, Federal Register, Investopedia

免責聲明:本文及其中任何文字均僅為一般性的介紹,絕不構成任何法律意見或建議,不得作為法律意見或建議以任何形式被依賴,我們對其不負擔任何形式的責任。我們強烈建議您,若有稅務問題,請立即諮詢專業的稅務律師或稅務顧問。

Disclaimer: This article and any content herein are general introduction for readers only, and shall not constitute nor be relied on as legal opinion or legal advice in any form. We assume no liability for anything herein. If you need help about tax, please talk to a tax, legal or accounting advisor immediately.