【2024.4更新】在文首添加了保險的方法,在總結前增加了safe harbor的定義辨析。

【2021.5更新】增加了修改示例一節,介紹修改W4增加withholding的具體操作步驟。

2020年/2021年股市大起大落,不少朋友有投資收入。然而股市收入不像W2工資收入那樣默認有預扣(withholding),盈利太多可能會造成欠稅,在來年收到了IRS信要求罰款。

美國目前的收入稅徵收方式是”pay as you go”,即在獲得收入的時刻應向聯邦政府履行納稅義務。

這個”pay as you go”系統一季度一結,下表是每季度的截止日期(payable in 4 installments, 26 U.S. Code Sec. 6654)

| Payment period | Due date |

| Jan. 1 – Mar. 31 | Apr. 15 |

| Apr. 1 – May. 31 | Jun. 15 |

| Jun. 1 – Aug. 31 | Sep. 15 |

| Sep. 1 – Dec. 31 | Jan. 15 of the following taxable year |

大部分讀者可能沒有聽說這些季度繳稅截止日期,只知道每年4月15日之前要報稅。這是因為W2收入是以僱主預扣稅(withholding)滿足要求。自雇收入,以及另外一些1099表格的收入,比如利息、股票收益等則沒有默認的預扣稅機制,需要以增加W2 withholding的方式,或者在當季繳estimated tax補足。不繳或遲繳有罰款。

本文詳細介紹withholding以及estimated tax的繳稅機制,讓大家在有工資之外收入的情況下避免罰款。 本文推薦的保險方法是

- 全年預扣稅(withholding) > 去年實際繳稅額 * 110%

若使用estimated tax (使用Form 1040ES),則要確保每一季度滿足

- 全年預扣稅(withholding) * 25% + 該季度estimated tax(Form 1040ES) > 去年實際繳稅額 * 27.5%

建議通讀全文理解原理。

Contents

Safe harbor

Withholding是按時交稅的常見手段。

為了不給公眾造成太多麻煩,26 U.S. Code Sec. 6654給withholding的繳稅方式提供了兩個便利:

- withholding不管在什麼時候繳,都可以默認按四季平均計算。(Sec. 6654 (g))

- 只要withholding滿足safe harbor,無論當前taxable year的稅負是多少,都無需繳納罰款。(Sec. 6654 (d)(1)(B))

Safe harbor,安全港條款,是指在法規中明確指定不違法的行為。

對於繳稅來說,safe harbor要求withholding大於下面的任何一個數字

- 今年實際繳稅額 – 1k

- 今年實際繳稅額的90%

- 去年繳稅額的100%(如果去年的AGI超過150k,則是去年繳稅額的110%)

即公式:

withholding > current year tax - 1k

or current year tax * 90%

or last year tax * 100% ( 110% for AGI > 150k )

滿足該safe harbor rule,如果今年的欠稅額是多少,都不會產生罰款。

Current/last year tax籠統地說是今年/去年在Form 1040上的總的繳稅數字。

由於Form 1040經常變動,查找的位置並不一樣。最安全的辦法是通過查閱Form 2210 Instrucution獲得準確位置。

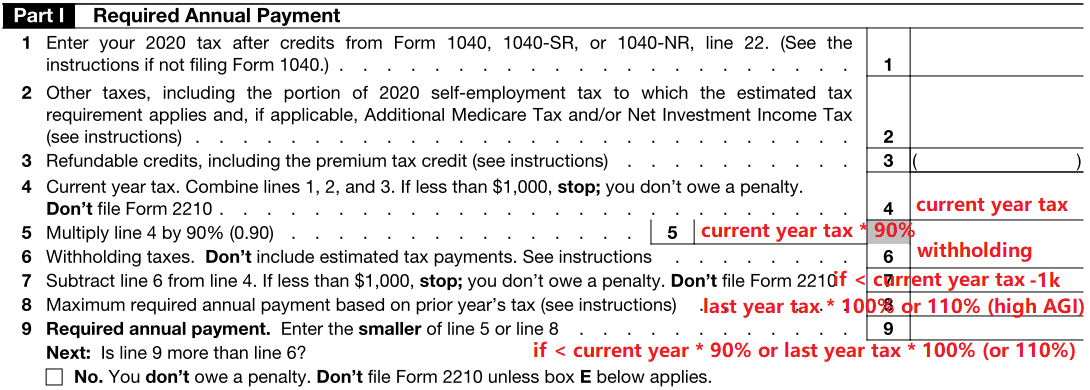

Form 2210

Form 2210用來計算沒有按時繳稅產生的罰款。

這張表格幾乎涵蓋了所有我們涉及的withholding以及estimated tax的問題。

想要了解細節的讀者請仔細研究一下。

本文呈現的是2020年報稅時的表格。

Part I用於驗證2020年納稅人是否滿足safe harbor rule,如圖

Line 4是計算出來的current year tax(即2020年)。對於沒有自雇收入以及tax credit的讀者來說,2020年的稅等於2021年報稅時Form 1040的Line 22。

Line 8,對於2020來說,去年的繳稅需要查詢2019的Form 1040 Line 14。(將這一行概括成去年繳稅額是一種簡化,其實還去掉了一些refundable credits。同時婚姻狀態在這兩年內改變也有較複雜的規則,詳見Form 2210 Instruction)。

紅字部分的計算復現了前述的safe harbor公式。滿足該公式的條件下,不需要繳納罰款,也不需要file Form 2210。

通常,current year tax只有在第二年報稅時才能精確知道,所以確保進入safe harbor的方式是,通過報前一年的稅得到精確的last year tax,然後讓今年的withholding滿足

withholding > 110% * last year tax

當然,假如能對current year tax有很好的預估,那麼使用safe harbor的另外兩個關於current year tax的條件可能預繳的稅更少。

有的讀者希望在及時足量的情況下,盡量減少withholding,因為錢有時間價值,在前幾個季度多上繳的稅相當於給IRS的無息貸款;有的讀者希望足量繳稅,這樣不需要擔心因為投資等其他波動收入影響擔心每季度是否繳夠。

這都可以通過Form W4精確調整每張paycheck的withholding。

Form W4 調整withholding

員工的收入、稅務狀態有變化時,可以向僱主提交Form W4修改每張paycheck的withholding。提交次數沒有限制,但月末提交可能下一張paycheck才能生效。

為了方便起見,下面的計算方法假設工資一月一付(兩周一付的原理相同)。Withholding即指每月的預扣稅。

修改步驟

- 默認的withholding

員工不主動提交W4,則僱主會以Publication 15-T的Worksheet 1計算默認的withholding。方法是把全年的工資在假設沒有任何deduction(包括standard deduction)的情況下,根據tax bracket計算得到一個數值。由於沒有考慮standard deduction,這個withholding的數值一般肯定比稅負高,所以大家每年的報稅季往往會有退稅。我們將這個計算過程表示為

withholding per month = P15T( total income )

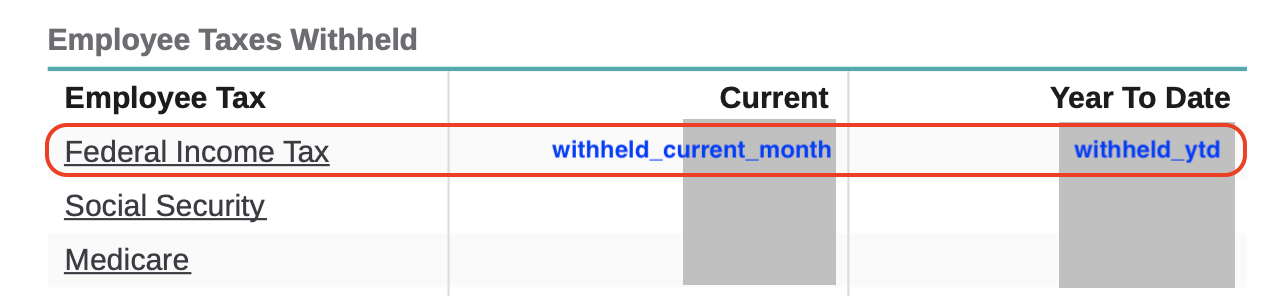

嫌麻煩的讀者也可以查看自己的paycheck stub,找到federal tax withholding類似的字樣,其中current表示這張paycheck的withholding數額。如果工資不是每月增長,則該數字即是公式中的withholding per month,如圖:

- 增加、減少withholding

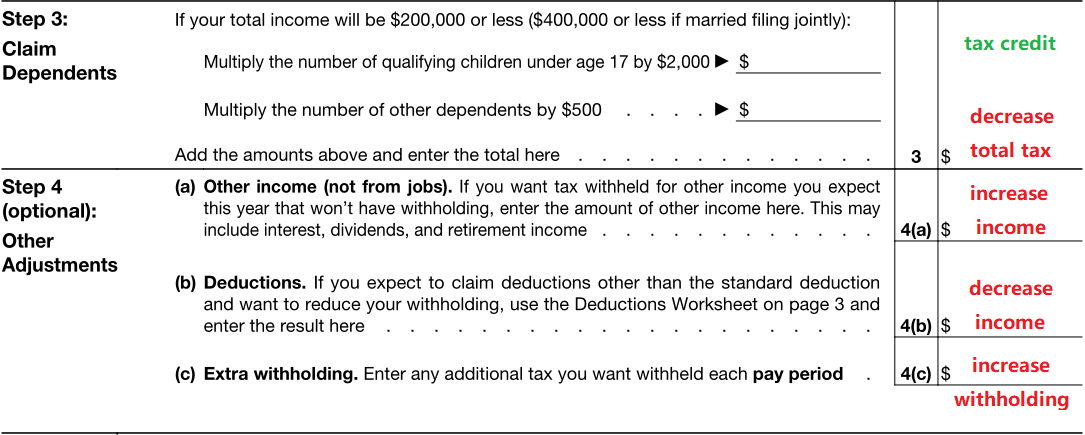

W4中有4個可以改變withholding,公式如下

withholding per month = P15T( total income + Line 4(a) - Line 4(b) ) - Line 3 / 12 + Line 4(c)

總結起來,Line 4(a)和4(b)分別增加或減少收入,Line 3是tax credit,減少了全年的稅負,而Line 4(c)增加了每月的withholding。

Line 3有隱藏選項。從Line 3的文字看,似乎必須有小孩或dependent才能填寫,但根據W4 instruction,Line 3也可以用來填其他的tax credit:

You can also include other tax credits in this step, such as education tax credits and the foreign tax credit. To do so, add an estimate of the amount for the year to your credits for dependents and enter the total amount in Step 3. Including these credits will increase your paycheck and reduce the amount of any refund you may receive when you file your tax return.

因此,如果沒有小孩或者dependent,則可以不填左邊的兩個空,只在Line 3中填寫tax credit。

這樣基本上能得到一個精確的withholding。事實上Publication 15-T的Worksheet 1的計算可以包含W4的這幾個Line。讀者可以填寫驗算,看withholding是否達到了想要的值。

有的僱主可以在線修改W4,一般是以網頁形式呈現Step 3和Step 4。填法和紙質的相同。

修改示例:增加withholding避免罰款

修改W4常見的功能是增加withholding,避免罰款。本例詳細解釋增加withholding進入safe harbor的方法。

前述safe harbor三個條件中最安全的是last year tax * 110% —— 這個數字在報稅完成即確定。對於2020年的withholding來說,需要以下幾個步驟:

- 完成2019年的報稅,在2019年Form 1040找到Line 14 (此位置可查詢Form 2210 Line 8 Instruction確認,一般為算完non-refundable credit之後的tax,以及加上schedule 2的一部分),此為last year tax。

- 查看最近一次收到的paycheck,找到withholding的current以及YTD值,如圖

其中current的值是withheld current month,即目前每月的預扣稅數額。而YTD則是從年初開始到目前總的預扣稅值withheld YTD。

假設這是今年第M張paycheck(例如4月1日收到的,可能是第4張,也可能是第5張),則每月需要增加的withholding數額為

extra withholding = ( last year tax * 110% - withheld YTD ) / ( 12 - M ) - withheld current month

註:AGI小於大約150k可使用last year tax * 100%

將第3步計算的extra withholding填到W4 Line 4(c)。

IRS計算器

IRS提供了在線的withholding 計算器。這個網頁以問卷方式計算預期的withholding以及tax refund。顯示結果後,可以調節預期的欠稅或退稅數額。滑動滑塊改變欠稅或退稅數額,則網頁會生成一個pre-filled W4供你提交。

當希望減小withholding時,網頁會生成的pre-filled W4,Line 3會寫有一個正的credit,這驗證了我們前面提到的Line 3不僅僅包含小孩與dependent credit,還可以是其他的tax credit。

Withholding補救措施 (W4/IRA)

W4可以提交任意次。如果withholding不夠,但還剩下多張paycheck,則可以通過前面例子中填寫W4的extra withholding在剩下的paycheck中補足。

如果遇到意外情況,沒有W2收入,且忘記按時繳estimated tax。此時可以用IRA withholding補足。假設需要補充10k withholding,方法如下:

從某IRA中取出10k,IRA的withholding數額可以自己填表選擇,此時要求券商100% withhold。然後在60天內往(同一個或另一個同類型的)IRA中存入10k。在稅務上,IRA withholding會與W2 withholding合併,都是默認全年平均計算。另一方面在60天內重新存入IRA則是完成了一次indirect rollover(見rollover詳解),不產生稅務後果。但注意indirect rollover每12個月只能做一次,超過將按照IRA distribution徵收稅與罰金。

按季度繳納Estimated Tax

另一種不通過withholding的方式是按季度繳estimated tax。

IRS提供了在線繳稅。其中有三家(PayUSAtax,Pay1040,ACI Payments, Inc.)可以以不超過2%的手續費用信用卡繳稅。每人每季度,在每個服務商可以繳兩次。

Withholding不管實際繳納時間,默認全年平均,estimated tax則是按每個季度實際的繳納數額計算。避免罰款需要滿足

estimated tax of Q1 + withholding this year * 25% > required annual payment * 25% estimated tax of Q1,Q2 + withholding this year * 50% > required annual payment * 50% estimated tax of Q1,Q2,Q3 + withholding this year * 75% > required annual payment * 75% estimated tax of Q1,Q2,Q3,Q4 + withholding this year * 100% > required annual payment * 100%

可見withholding默認平均,加上estimate tax,每個季度都要繳足required annual payment的25%,多繳的可以用來滿足剩餘季度的條件。其中required annnual payment是safe harbor中的後兩個條件

required annual payment = current year tax * 90% or last year tax * 100% ( 110% for high AGI )

保證withholding + estimated tax每季繳納不少於上年稅負的27.5%可以避免罰款。

有的時候,收入在第四季度非常多,按照前三季度收入的estimated tax繳稅,可能達不到required annual payment。此時只有在第四季度多繳,然後使用Form 2210的regular method驗算是否有罰款。Regular method可選擇使用schedule AI將收入annulized,得到每一季度的等效收入以及應繳稅款,並與該季度的withholding + estimated tax做比較。收入在四季分佈不均的讀者(特別是年尾收入多的),請詳細研究Form 2210 regular method和schedule AI計算的應繳稅款。

最後Sec. 6513 (d)規定overpayment可以在報稅時可以選擇一部分充當下一年的estimated tax。因是前一年繳納的,作為estimated tax時算在第一季度。

Estimated tax可否代替withholding?

Estimated tax可以使用信用卡支付。本博客讀者自然會有人問能否用W4將withholding改成0,然後使用信用卡支付estimated tax獲得額外的點數和積分,本站有介紹。

我個人認為,該行為並沒有違法稅法。根據26 U.S. Code Sec. 3402, 僱主應根據員工的收入水平做withholding。但26 U.S. Code Sec. 6682指出了例外情況,在withholding不足的情況下,用estimated tax繳足可以免於罰款。

Reddit的繳稅帖子對給問題的回答是不建議:

Q. Should I bump up my W-4 withholdings, and make all my tax payments this way?

…

The IRS does check and make sure everyone is making the right estimated tax payments. If your withholdings look unreasonable, the IRS can contact your employer to ask them to correct it. So you should not do this. Work it out with your tax accountant to get professional advice.

讀者如果仍然希望嘗試,則注意3點

- Form W4 需要納稅人”under the penalty of prejuries”確認所填寫的內容屬實。讀者填寫的deduction和tax credit要在合理範圍能解釋。

- 雖然目前IRS不要求僱主定時提交員工的W4,一個只有W2收入的納稅人,其1040上顯示的federal tax withheld = 0,是否會引起IRS的額外注意不得而知。

- 交estimated tax務必注意截止日期。因為estimated tax嚴格按照季度分配,錯過了截止日期而不用withholding補足則幾乎必然導致罰款。假如每季度繳款不是均勻的,則應檢查是否需要File Form 2210(只有計算結果有罰款,或使用regular method + schedule AI時才需要)。

注: safe harbor 名詞辨析:文本將safe harbor定義為Form 2210的Part I,即withholding大於以下任意一個:

- current year tax – 1k

- current year tax * 90%

- last year tax * 100% or 110% (high AGI)

此時完全不用考慮季度要求。

另一種常見的理解是將safe harbor理解為條件2或條件3。此時應若用withholding + estimated進入safe harbor(即滿足條件2或條件3),除了總量滿足外,還需要考慮季度要求。讀者應根據上下文識別safe harbor的含義。

總結

本文詳細介紹了使用withholding與estimated tax按時足額繳稅的方法。

最安全的進入safe harbor的方法是利用前一年的繳稅額:

- withholding this year > last year tax * 110%

如果使用estimated tax,則要確保每一季度

- withholding this year * 25% + estimated tax this quarter > last year tax * 27.5%

Withholding最大的好處是默認全年平均以及容易控制的safe harbor rule。每月的withholding數額可以通過Form W4精確調整。使用estimated tax方式繳稅則不要錯過了每季度的截止日期。複雜的情況請仔細研究Form 2210。

參考資料:Publication 505, Form 2210 Instruction, Publication 15-T, Kitces, Money Stackexchange

免責聲明:本文及其中任何文字均僅為一般性的介紹,絕不構成任何法律意見或建議,不得作為法律意見或建議以任何形式被依賴,我們對其不負擔任何形式的責任。我們強烈建議您,若有稅務問題,請立即諮詢專業的稅務律師或稅務顧問。

Disclaimer: This article and any content herein are general introduction for readers only, and shall not constitute nor be relied on as legal opinion or legal advice in any form. We assume no liability for anything herein. If you need help about tax, please talk to a tax, legal or accounting advisor immediately.