Update: 更新留学生的特殊Closer Connection Exception,不再有183天的限制。感谢读者chenyuetian提供的链接:

https://www.irs.gov/individuals/international-taxpayers/the-closer-connection-exception-to-the-substantial-presence-test-for-foreign-students

根据此链接,作者也去对应法规Internal Revenue Code section 7701(b)(5)(D) and (E) and in Treas. Reg. § 301.7701(b)-3(b)(7)(iii) 查阅了一番,对于留学生这个群体,有另一种特殊的exception:

- does not intend to reside permanently in the United States; 容易证明

- has substantially complied with the immigration laws and requirements relating to his student nonimmigrant status; 容易证明

- has not taken any steps to change his nonimmigrant status in the United States toward becoming a permanent resident of the United States; and 容易证明

- has a closer connection to a foreign country than to the United States as evidenced by the factors listed in Treasury Regulation 301.7701(b)-2(d)(1). 主观性强

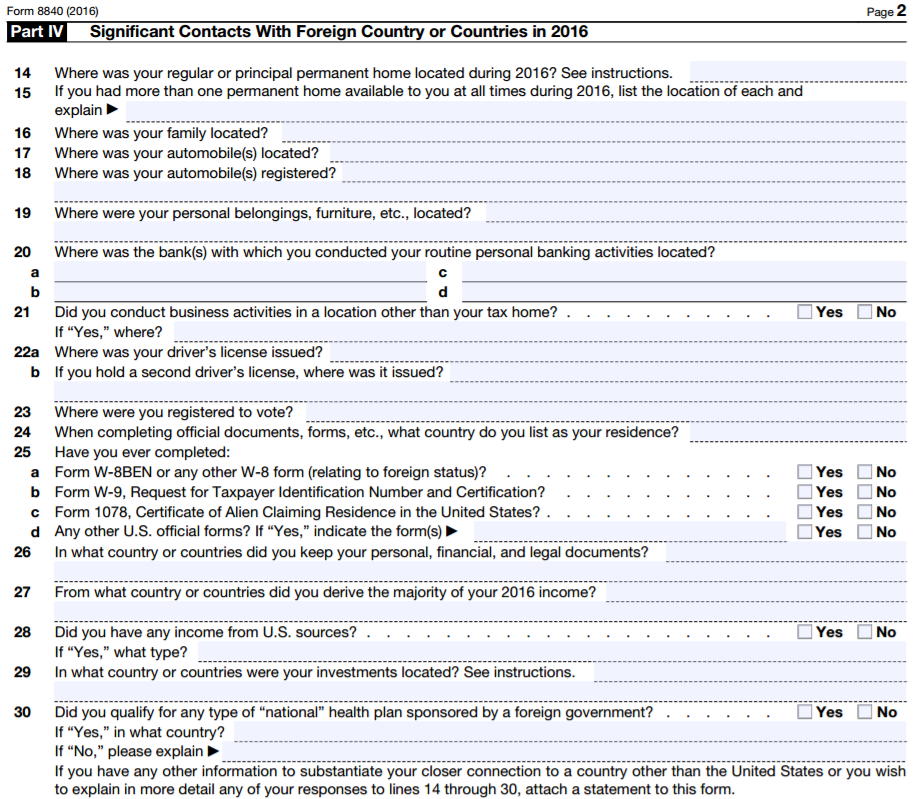

文末也提到:The burden of proof is on the student to prove these four factors. 证明满足所有条件的义务在学生自己,而不在IRS。8843表的Line 12有要求附上一份statement来解释超过5年的情况。关于第四点的factors在正文有提到,大家也可以参考Form 8840的Part IV Significant Contacts With Foreign Country or Countries,来评估自己的情况。

最后,作者想说,其实这个问题怎么回答都是可以的,如果按照经验主义来说,税局是极少在留学生报税身份上较真的,而且正文开头也已经说到按resident报税好处也是不少的。所以请各位看官一笑了之。从个人从业经验来看,省税是一方面,省事也是一方面,大家多多权衡。

最后,作者想说,其实这个问题怎么回答都是可以的,如果按照经验主义来说,税局是极少在留学生报税身份上较真的,而且正文开头也已经说到按resident报税好处也是不少的。所以请各位看官一笑了之。从个人从业经验来看,省税是一方面,省事也是一方面,大家多多权衡。

时光飞逝,有没有感觉一眨眼,留学美国已经多年过去?这个时候你就要注意了,从税务的角度你可能已经和美国居民一视同仁,成为 Resident Alien (RA) 了。如果你对 RA 和 NRA 还不了解,请移步我们的《报税身份辨析》。在你理解了 Substantial Presence test 之后,你会说我们在美国仅仅一年就超过了183天。请注意之所以留学生可以不受这个的影响,是因为持F签证等的留学生属于“Exempt individual”,这样的话天数是不算入test里的。但是这个是只有五年的(5 calendar years),在你来美的第六年就要开始计算天数了。

那是不是超过5年之后,满足 Substantial Presence test 的 F1身份的人就必须要按照 Resident Alien 来报税呢?下文将慢慢分解。

首先,有人可能会问,为什么有人会想要维持 Nonresident 身份呢?其实从报税的角度,按照 Resident 报税能够带来更多的好处:夫妻报税,增加dependent,standard deduction 或者更丰富的 itemized deduction 等等。当然,前提是你没有很多的海外收入。美国的 Resident 和绿卡持有者或者公民一样,都是全球征税的,而且还有霸气无比的法案 FATCA 的存在让监管变得很严格。如果有海外收入,这个确实需要进一步考量,甚至牵扯到 foreign earned income exclusion 或者 foreign tax credit,不属于本文范围。(你或许会说,Nonresident 还有$5,000的treaty可以抵税呢,那么下次,我就来跟大家说说超过五年还能不能用treaty的问题。)

接下来就讲讲 Resident Alien 判定标准的例外情况。

我们来看看Publication 519, U.S. Tax Guide for Aliens的原文:

You will not be an exempt individual as a student in 2016 if you have been exempt as a teacher, trainee, or student for any part of more than 5 calendar years unless you meet both of the following requirements.

- You establish that you do not intend to reside permanently in the United States.

- You have substantially complied with the requirements of your visa.

从这段看,如果你满足没打算永久居留美国并且严格服从签证要求,那么你还是可以做“Exempt individual”的,维持 Nonresident Alien 的身份。看起来并不难,对吧?

别急,我们继续:

The facts and circumstances to be considered in determining if you have demonstrated an intent to reside permanently in the United States include, but are not limited to, the following.

- Whether you have maintained a closer connection to a foreign country (discussed later).

- Whether you have taken affirmative steps to change your status from nonimmigrant to lawful permanent resident as discussed later under Closer Connection to a Foreign Country.

第二个好理解,有没有开始永久居民的申请,这个一般还在读书或者刚毕业还遇不到,那么第一条 Closer Connection to a Foreign Country,怎么证明呢?是不是家人在国内,就足以了呢?在后文有专门介绍Closer Connection to a Foreign Country的,我们简单看一下基本要求:

Even if you meet the substantial presence test, you can be treated as a nonresident alien if you:

- Are present in the United States for less than 183 days during the year,

- Maintain a tax home in a foreign country during the year, and

- Have a closer connection during the year to one foreign country in which you have a tax home than to the United States (unless you have a closer connection to two foreign countries, discussed next).

因为这里用的是“and”,所以三个要求都要满足。第一个要求,在美不超过183天!仅此一点,大多数朋友都不满足了吧。。。

至于另外两项,则是比较棘手而且主观的问题,是需要在审查时你需要像税局证明的,这其中牵扯到很多因素,工作地方、人际圈、生活圈等等。没有一个简单化一的标准答案,而是综合考量的结果(和bona fide resident的判断有点像,这个是绿卡持有人在海外工作会常常遇到的,以后再谈)。

附上税局给的一段list,以供参考。

In determining whether you have maintained more significant contacts with the foreign country than with the United States, the facts and circumstances to be considered include, but are not limited to, the following.

1. The country of residence you designate on forms and documents.

2. The types of official forms and documents you file, such as Form W-9, Form W-8BEN, or Form W-8ECI.

3. The location of:

a. Your permanent home,

b. Your family,

c. Your personal belongings, such as cars, furniture, clothing, and jewelry,

d. Your current social, political, cultural, professional, or religious affiliations,

e. Your business activities (other than those that constitute your tax home),

f. The jurisdiction in which you hold a driver’s license,

g. The jurisdiction in which you vote, and

h. Charitable organizations to which you contribute.

It does not matter whether your permanent home is a house, an apartment, or a furnished room. It also does not matter whether you rent or own it. It is important, however, that your home be available at all times, continuously, and not solely for short stays.

可以看出,须考量的方面非常广,据我所知,甚至包括驾照、图书卡、协会活动等等。

综上,想要在五年以后继续维持 Nonresident,所需条件在天数上就被卡住了,哪怕没有,后面的判定上也会比较头疼。

参考链接:https://www.irs.gov/pub/irs-pdf/p519.pdf

Caiwade,注册会计CPA,致力于中国留学生和移民的税务普及和答疑解惑。