In the previous post we showed the general concepts of credit score and credit history and specifically mentioned that FICO credit score was most authentic important to you. This post is going to figure out how is FICO credit score calculated.

Contents

Overview

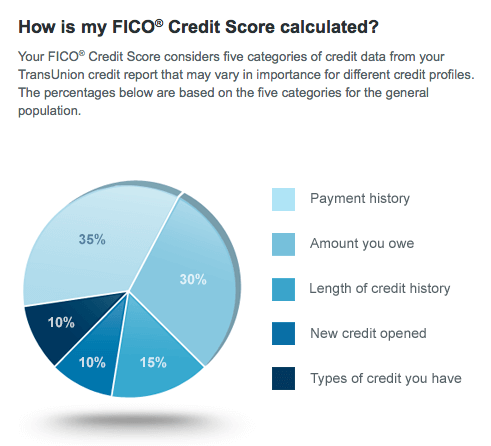

The most widely used FICO model is FICO 8 in which the percentages of the credit score are listed blow:

1. Payment History: 35%

It is your loan/debt payment history. For credit card, when the billing statement comes out every month, the bank will set a minimum payment. As long as you pay at least the minimum payment before the due date, the bank would report an OK to credit bureaus. I strongly suggest you fully pay the statement, or which will cost you money in the form of interest.

To ensure timely payment, it’s better to set auto payment in case you were too busy to forget about that. If it’s the first time to pay late, you can try to call the bank to beg for mercy and let them not report it to credit bureaus.

2. Credit Limit and Utilization Rate:30%

Utilization rate is the amount you owe compared to your credit limit. It is used to monitor your economic situation. If the utilization rate always keeps low, which illustrates you’re out of payment crisis, you of course are creditable. During the calculation, rates of both a single credit card and all will be taken into consideration, but all in all, the latter is more important.

We suggest you take full strength to control the utilization rate under 10%, no more than 50% for one card too. For example, if there were two credit cards with credit limits of $1,000 and $3,000 respectively, and the total limit is $4,000, I had to keep the total payment under $400. For these two cards, it would be better to set limits of $500 and $1500 respectively (the targeted amount is lower than them two).

As for newbies, because they have only one or two cards with very low credit limit, they are required to pay their payments frequently and make sure statement balances under the limit said above before the statements come out. Their statement balances will be reported to credit bureau by the banks. Then according to these statistics, the credit bureau will calculate their utilization rates. When the cards are increased and limits lifted in the future, it is no need for them to fill the payment so often.

3. Credit History Length: 15%

Credit history length includes the longest history length and average history length, while the former is calculated according to your first credit card. That’s why, at the last posts, we strongly suggested your first credit card be free from annual fee. Besides, to hold a card like that, in the long term, is free from worries. All you should do is to use it sometimes in case it was canceled by the bank because of inactivity.

4. New Credit Opened: 10%

There are two factors: new account and Hard Pull (HP).

Every time when you apply for a credit card, the bank will ask one or two credit bureaus for your credit report, which is called hard pull, and it will be recorded in your credit history. Whether or not your application is approved, hard pull is there. So we suggest you, especially the newbies, should think it twice before you apply for a card.

As your application is approved, the bank will naturally report that account to credit bureau. And this account which is just open and has short history length is named new account.

If one in a short period was crazy for new credit cards or new loans, the bank might worry about it and think he was dropped in financial issues, which at last, to some degree, would have some impacts on his credit. But as you all know it accounts only for 10%, its effect doesn’t go deep.

5. Types of Credit: 10%

If you are able to well deal with your student loan, car loan and credit card at the same time, it illustrates you’re capable. Your ability will be shown here to manage different accounts. Generally, the most you guys have would be credit card and car loan. Timely payment is the only request.

Credit score range

I almost forgot the key point and have typed so many words above. Generally, FICO score ranges from 300 to 850:

- 300-579: Too low. It means you’ve great risk in debt. Usually, the credit report reads you’ve serious credit issues.

- 580-669: Low. Some risk factors are written in the credit report, such as high late payments.

- 670-739: Average. Most people are located in this range. Generally, no worries.

- 740-799: Good. You have nice credit history. No restrictions at all. XDDD.

- 800-850: Excellent. No limits to apply for credit cards.

I have had 19 credit cards till now. The longest history length is 1.8 years with an average length of 0.8. My FICO scores in three credit bureaus are listed blow:

- Experian: 727,19 HP

- Equifax: 761,4 HP

- TransUnion: 741,7 HP

It can be seen that differences really exist. Because report of Experian is regularly been used now when apply for credit cards, HP in Experian is much more than the other bureaus. Differences in HP do affect the credit scores, but as a whole, my scores are all in good standing. So the key for high credit score is not the amount of HP but a good habit to manage your cards. Tomorrow I’ll write another post: Boosting Your Credit Score by Paying Correctly!