One of the perks of Amex MR is the convenient way to cash out at 1.25 cents/point using Schwab Platinum card. Unfortunately, there have been rumors recently that Schwab will cancel this benefit in the near future.

Seeking to exploit the last opporunity, frequentmiler blogger suggested to cash out MR into a Roth IRA, rather than a brokerage account. This action has an additional benefit of expanding the Roth contribution limit. As discussed on Reddit that Schwab will label the contribution as 「account incentives」, rather than the Roth IRA contribution reported to the IRS. Thus, the route MR->Schwab Platinum->Roth IRA appears to effectively break the Roth IRA annual contribution limit set by the tax code.

We analyze the tax consequence of this operation in the format of Q&A. Our conclusion is that we do not recommend this operation, either for the purpose of expanding the Roth space, or doing regular Roth contribution.

For simplicity, we will not regard this operation as the intermedia procedure of an indirect rollover.

Contents

- Q: Is MR->Schwab Platinum->Roth IRA regarded a Roth IRA regular contribution?

- Q: If Schwab does not report it as regular contribution, it should be legal to do so?

- Q: OK, if the IRS finds out,what would be the consequences?

- Q: So 6% penalty, in exchange of the enlarged Roth space, would you recommend it?

- Q: But I still want to do it, can you give me some supportive opinion?

- Summary

Q: Is MR->Schwab Platinum->Roth IRA regarded a Roth IRA regular contribution?

A: We believe the answer is yes, according to the tax code.

Without considering rollover, there are two parts in the Roth IRA accounting for the tax purposes:

| Roth IRA | Source |

| regular contribution | cash deposit |

| earnings | gain/loss within Roth IRA |

The regular contribution is what you directly deposite into the Roth IRA in the form of cash, which is subject to the annual contribution limit. The earnings are what remains — it is the gain or loss resulting from the investment inside the Roth IRA.

The MR, either from rebate or account openning bonuses, are benefits outside the Roth IRA investiments. Therefore they can in no way be treated as Roth IRA earnings.

There could be exceptional cases. For example, if the MR are the bonuses of opening Schwab Roth IRA, or the gain of a particular investiment inside Roth IRA, then they are Roth earnings. An analogous (and conventional) example is the cash bonus of opening an IRA. The cash bonus is not a Roth IRA regular contribution, rather it is treated as the income deriving from opening and depositing funds into the Roth IRA, and therefore is the gain. Obviously, MR is obtained through the business with American Express, not the Roth IRA investments under the custody of Charles Schwab. These exceptions do not apply.

One thing to note is that MR can not be directly deposited into Roth IRA. This is because the only way to make regular contribution is through cash or its equivalent(IRC Sec. 408(a)(1)). So for tax purposes, cashing out MR into a Roth IRA contains two steps:

- MR -> cash outside Roth IRA via Schwab Platinum

- cash -> Roth IRA

If the total amount exceeds the annual contribution limit, the excess amount is the excess contribution of the Roth IRA. This results in penalties that we discuss below.

Q: If Schwab does not report it as regular contribution, it should be legal to do so?

A: According to our analysis above, Schwab should report this contribution on Form 5498 after each tax season when the total contribution amount is determined. Form 5498 will be sent to IRS and the IRA owner, informing both parties the nature of this transaction. Yet, data points show that this is not the case. Schwab, due to various reasons, does not report this contribution on Form 5498, and the IRS is unaware of this transaction through the means of Form 5498.

However, we emphasize that the tax forms provided by the third party such as the brokerage firm are only meant to assist the taxpayer. It is the taxpayer who has the liability (and information) to classify the nature of all the transactions (taxable/non-taxable, Roth basis or earnings etc.), and report on the tax form. Once the IRS finds out the transactions of depositing excessive amount of MR into a Roth IRA, Schwab may not be liable for this operatration; the taxpayer will be. And there will be penalties retrogressively for the passing years.

Q: OK, if the IRS finds out,what would be the consequences?

A: The IRS can certainly find out throught the transaction history of the Roth IRA, although they do not monitor it regularly. They could request taxpayer to prove that this transaction (depositing MR) is not a regular contribution, should they find any suspicious behaviors.

There is a 6% excise tax (penalty) for each year the excess contribution remains inside the Roth IRA. Note it is 6% of the excess contribution, not 6% of the gain deriving from it.

Q: So 6% penalty, in exchange of the enlarged Roth space, would you recommend it?

A: We do not recommend this operation.

If it is within the annual contribution limit, the contribution by depositing MR will not be reported by Schwab. Thus from the IRS persective, it is not a regular contribution. Remember, the regular contribution of Roth IRA can be withdrawn at any time without tax or penalty (return of basis). You do not want to lose that status by the Schwab’s erroneous reporting.

If it exceeds the annual contribution limit, then there are chances that the IRS will find out and retrogressively collect the 6% excise tax for each year.

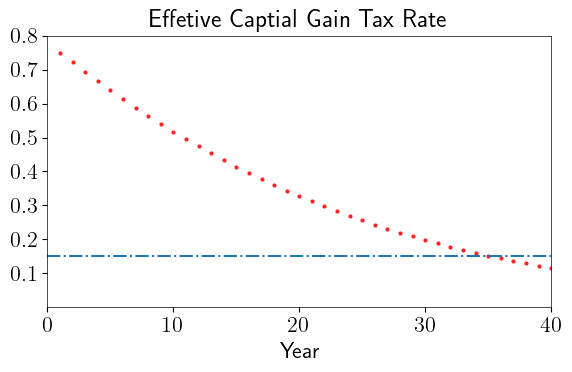

Let us do a simple calculation to see if it is worth the benefit of tax free withdrawal of the earnings. Assumming the excess contribution to be M, then the excise tax for Y years is

M * 6% * Y

Assuming an 8% annual growth rate of the investments (the SP 500 value), the gain for Y years is

M * ( 1 + 8% )^ Y - M

If we regard the excise tax as an effective captial gain tax, then then rate is

6% * Y / ( ( 1 + 8% )^ Y - 1 )

We have ploted the effective rate vs the number of years of paying the penalty. It takes more than 30 years to reduce the effective rate below 15% — the current long term captial gain rate. It takes more than 20 years to reduce it below even 30%. And you cannot control the number of years. The IRS may start to collect the penalty next year. We think this is not a good deal.

On top of this, there are costs of dealing with IRS, and their additional attention on your tax form due to this challenge. Therefore we do not recommend any form of excess contribution. Even if you want to deliberately break the law and pay the excise tax, it is not worth it.

Q: But I still want to do it, can you give me some supportive opinion?

A: Some people believe it is legitmate, see reddit discussion。

They are not tax/legal professionals, neither am I.

Proceed on your own risk.

Summary

We analyze the tax consequence of cashing out MR into the Roth IRA, and categorize it as regular Roth contribution.

We do not recommend this operation, even though Schwab does not appear to report this contribution on Form 5498. The annual 6% excise tax imposed on the excess contribution outweighs the benefits of avoiding the 15% long term captial gain tax, rendering this strategy not so useful.

Please consult a tax/legal expert if you insist on using this strategy.

Reference :frequentmiler comment section

Disclaimer: This article and any content herein are general introduction for readers only, and shall not constitute nor be relied on as legal opinion or legal advice in any form. We assume no liability for anything herein. If you need help about tax, please talk to a tax, legal or accounting advisor immediately.